New York State taxes are among the most intricate tax systems in the United States, affecting residents, businesses, and even non-residents in various ways. Whether you’re a newcomer to the state or a long-time resident, understanding the nuances of New York’s tax structure is crucial for financial planning and compliance. This article dives deep into the key aspects of New York State taxes, including income tax rates, sales tax, property tax, and other important considerations. By the end, you’ll have a clearer picture of how these taxes impact your wallet and how to navigate them effectively.

The tax landscape in New York is constantly evolving, with regular updates to laws and regulations. Staying informed about these changes can help you avoid costly mistakes and take advantage of available deductions and credits. From individual taxpayers to small business owners, everyone in New York must comply with state tax requirements, making it essential to stay up-to-date with the latest information. This guide aims to simplify the complexities of New York State taxes and provide actionable insights for better financial management.

As we explore the intricacies of New York State taxes, it’s important to note that the state’s tax system is designed to fund public services, infrastructure, and other critical needs. However, for taxpayers, it can sometimes feel overwhelming due to its complexity. By breaking down the different components and offering practical advice, this article will empower you to make informed decisions about your finances and ensure compliance with state tax laws.

Read also:Aagmal A Thrilling Web Series Thatrsquos Capturing Hearts Worldwide

What Are the Key Components of New York State Taxes?

New York State taxes encompass a wide range of categories, each with its own rules and regulations. The primary components include income tax, sales tax, property tax, and excise tax. Understanding how each of these taxes works is essential for managing your financial obligations effectively. For instance, income tax rates in New York are progressive, meaning they increase as your income rises. This ensures that higher earners contribute a larger share to state revenues.

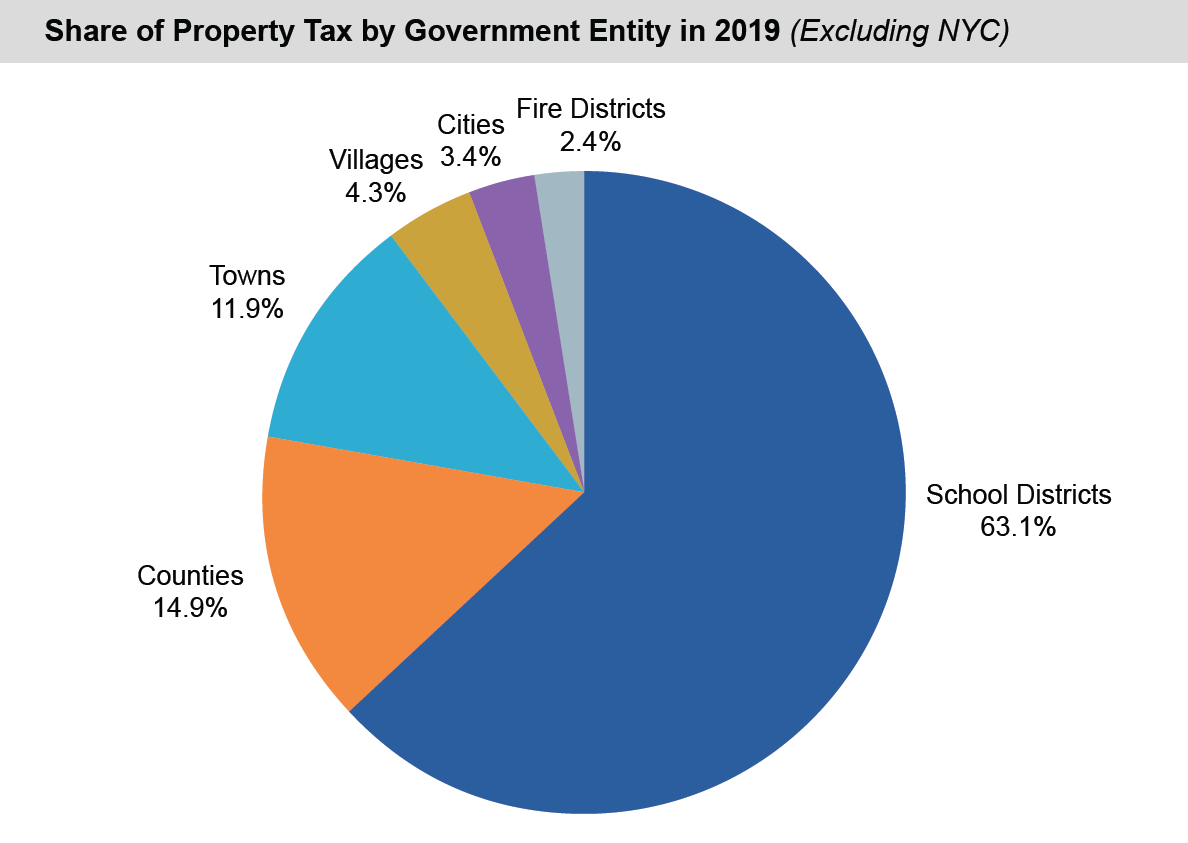

Sales tax, on the other hand, applies to most goods and services purchased within the state. While the standard rate is set by the state, local jurisdictions may add their own surcharges, resulting in varying rates across different areas. Property tax, another significant component, is levied on real estate and can vary significantly depending on the location and value of the property. Lastly, excise taxes target specific goods and services, such as gasoline, alcohol, and tobacco products.

How Do New York State Taxes Impact Residents?

Residents of New York are subject to a variety of state taxes that can have a substantial impact on their finances. For example, the progressive income tax structure means that as your income increases, so does the percentage of tax you owe. Additionally, the state’s high sales tax rate can add up quickly, especially for those who frequently make purchases. Property owners also face significant property tax burdens, which can vary widely depending on the location and value of their property.

To mitigate these impacts, it’s important for residents to take advantage of available deductions and credits. The New York State tax code includes numerous provisions that can reduce your tax liability, such as the Earned Income Tax Credit (EITC) and various itemized deductions. By staying informed about these opportunities, you can minimize the financial burden of New York State taxes.

Why Are New York State Taxes So Complex?

The complexity of New York State taxes stems from the state’s need to address a wide range of fiscal requirements. With a large and diverse population, New York must fund numerous public services, infrastructure projects, and social programs. This has led to the development of a tax system that is both comprehensive and intricate, with numerous rules and exceptions.

For example, the state’s income tax brackets are designed to ensure fairness by taxing higher earners at a higher rate. However, this also means that taxpayers must carefully calculate their income to determine the appropriate tax rate. Similarly, the varying sales tax rates across different jurisdictions can make it challenging for businesses and consumers to keep track of their tax obligations. Understanding the reasons behind this complexity can help taxpayers navigate the system more effectively.

Read also:Unveiling The World Of Kannada Cinema A Comprehensive Guide To 4 Movierulz Kannada 2024

Who Needs to Pay New York State Taxes?

Not everyone is subject to New York State taxes, but the majority of residents and businesses within the state must comply with its tax requirements. This includes individuals who earn income in New York, regardless of where they live, as well as businesses that operate within the state. Non-residents who work in New York may also be required to pay state income tax on their earnings.

For businesses, the tax obligations can be even more complex, depending on the type of business and its activities. Corporations, partnerships, and sole proprietorships all have different tax requirements, and it’s important for business owners to understand their obligations to avoid penalties and legal issues. By identifying who needs to pay New York State taxes, this guide aims to clarify the responsibilities of different taxpayers.

Can You Avoid New York State Taxes?

While it’s impossible to completely avoid New York State taxes, there are legitimate ways to reduce your tax liability. One of the most effective strategies is to take advantage of available deductions and credits. For example, the New York State tax code includes provisions for itemized deductions, such as mortgage interest and charitable contributions, which can significantly lower your taxable income.

Additionally, certain credits, such as the Child Tax Credit and the Elderly or Disabled Credit, can further reduce your tax burden. It’s important to note that attempting to evade taxes through illegal means can result in severe penalties, including fines and imprisonment. Therefore, it’s always best to work within the framework of the law to minimize your tax obligations.

How Much Are New York State Taxes?

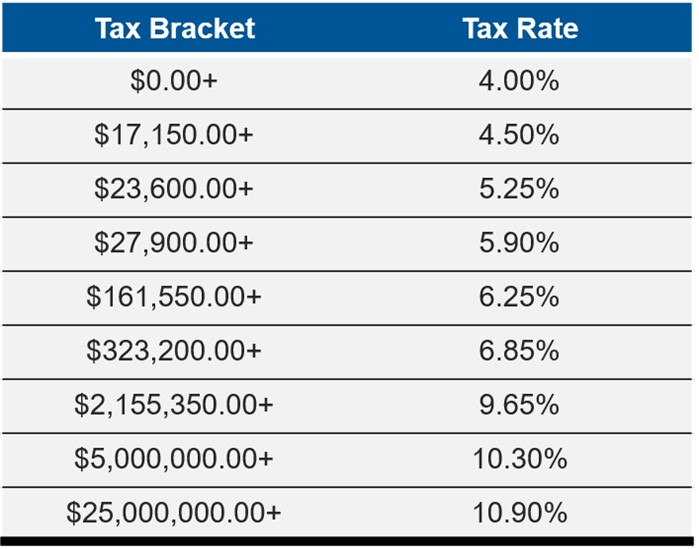

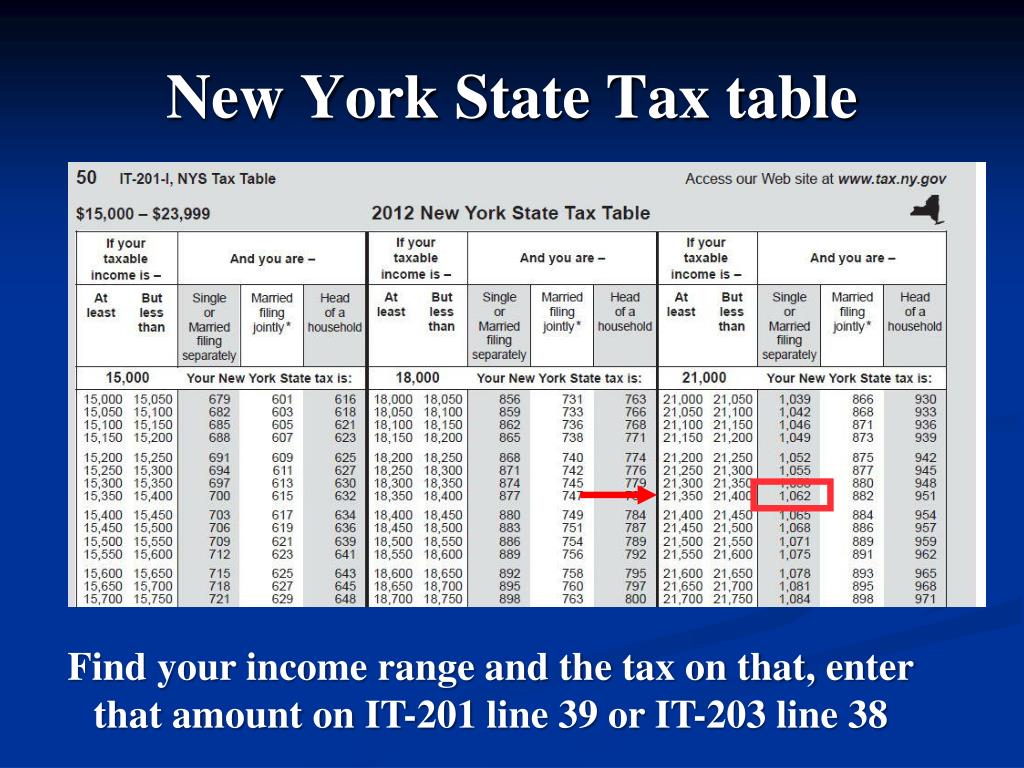

The amount of New York State taxes you owe depends on several factors, including your income, the type of property you own, and the goods and services you purchase. Income tax rates in New York are progressive, with rates ranging from 4% to 10.9% for the 2023 tax year. This means that higher earners will pay a larger percentage of their income in taxes.

Sales tax rates vary across the state, with the statewide rate set at 4%, and additional local surcharges bringing the total rate as high as 9% in some areas. Property taxes, on the other hand, are assessed based on the value of your property and can vary significantly depending on your location. By understanding these rates and how they apply to your situation, you can better plan for your tax obligations.

What Are the Deadlines for New York State Taxes?

Knowing the deadlines for New York State taxes is crucial for ensuring timely compliance and avoiding penalties. For individual taxpayers, the deadline for filing state income tax returns is typically April 15th, aligning with the federal tax deadline. However, if you need more time to prepare your return, you can request an extension by filing Form IT-201.

Businesses have different deadlines depending on their structure and activities. Corporations, for example, must file their returns by March 15th, while partnerships and S corporations have a deadline of April 15th. It’s important to note that extensions are available for businesses as well, but they must be requested in advance. Staying aware of these deadlines can help you avoid costly penalties and maintain good standing with the state.

What Are the Penalties for Late Payment of New York State Taxes?

Failure to pay New York State taxes on time can result in significant penalties and interest charges. The state imposes a late payment penalty of 0.5% of the unpaid tax for each month or part of a month that the tax remains unpaid, up to a maximum of 25%. In addition to this penalty, interest is also charged on the unpaid balance at a rate determined by the state.

For businesses, the penalties can be even more severe, with additional fines for late filing or failure to remit required payments. It’s important to prioritize timely payment of New York State taxes to avoid these costly consequences. By understanding the penalties and taking proactive steps to meet your obligations, you can protect your financial well-being.

What Should You Do If You Can’t Pay New York State Taxes?

If you find yourself unable to pay your New York State taxes on time, there are options available to help you manage the situation. The state offers installment payment plans, which allow you to pay your tax liability in smaller, more manageable amounts over time. To qualify for an installment agreement, you must file all required tax returns and meet certain criteria.

In some cases, you may also be eligible for hardship relief, which can provide temporary relief from penalties and interest. It’s important to contact the New York State Department of Taxation and Finance as soon as possible to discuss your options and find a solution that works for your financial situation. By addressing the issue proactively, you can avoid more severe consequences down the road.

Where Can You Get Help with New York State Taxes?

Navigating the complexities of New York State taxes can be challenging, but there are resources available to help you. The New York State Department of Taxation and Finance offers a wealth of information on its website, including tax forms, publications, and FAQs. Additionally, you can reach out to their customer service team for assistance with specific questions or issues.

For more personalized guidance, consider consulting with a tax professional or accountant who specializes in New York State taxes. These experts can help you understand your obligations, identify potential deductions and credits, and ensure compliance with state tax laws. By leveraging these resources, you can gain peace of mind and confidence in managing your tax responsibilities.

What Are the Latest Updates on New York State Taxes?

The tax landscape in New York is constantly evolving, with regular updates to laws and regulations. Keeping up with these changes is essential for staying compliant and taking advantage of new opportunities. Recent updates include adjustments to income tax brackets, changes to sales tax rates in certain jurisdictions, and the introduction of new credits and deductions.

For example, the state recently expanded eligibility for the Earned Income Tax Credit, making it easier for more taxpayers to qualify. Additionally, new rules for remote workers have been implemented to address the challenges posed by the increasing prevalence of telecommuting. By staying informed about these updates, you can ensure that your tax strategies remain effective and compliant.

How Can You Plan for New York State Taxes?

Proactive planning is key to managing your New York State tax obligations effectively. Start by keeping detailed records of your income, expenses, and deductions throughout the year. This will make it easier to prepare your tax return and identify potential credits and deductions. Additionally, consider setting aside a portion of your income to cover estimated tax payments if you’re self-employed or receive income not subject to withholding.

For businesses, it’s important to establish a reliable accounting system and work closely with a tax professional to ensure compliance with all state tax requirements. By taking these steps, you can minimize your tax liability and avoid costly mistakes. With careful planning and attention to detail, you can navigate the complexities of New York State taxes with confidence.

Conclusion

In conclusion, understanding New York State taxes is essential for anyone living or doing business in the state. From income tax to sales tax and property tax, each component plays a vital role in funding public services and infrastructure. While the system may seem complex, there are numerous resources and strategies available to help you manage your tax obligations effectively.

By staying informed about the latest updates, taking advantage of available deductions and credits, and seeking professional guidance when needed, you can ensure compliance and minimize your tax burden. Remember, proactive planning and attention to detail are key to navigating the intricacies of New York State taxes successfully.

Table of Contents

- What Are the Key Components of New York State Taxes?

- How Do New York State Taxes Impact Residents?

- Why Are New York State Taxes So Complex?

- Who Needs to Pay New York State Taxes?

- Can You Avoid New York State Taxes?

- How Much Are New York State Taxes?

- What Are the Deadlines for New York State Taxes?

- What Are the Penalties for Late Payment of New York State Taxes?

- What Should You Do If You Can’t Pay New York State Taxes?

- Where Can You Get Help with New York State Taxes?