New York taxes are among the most complex and scrutinized in the United States. From state income taxes to local property levies, the financial landscape for residents and businesses is intricate and ever-evolving. Understanding these obligations is not just a matter of compliance but also a strategy for optimizing financial health. Whether you're an individual filing your annual returns or a business owner navigating corporate taxation, staying informed about the latest regulations is crucial. This article delves into the nuances of New York's tax structure, offering actionable insights and expert advice to help you navigate the system effectively.

Living or operating in New York means facing a unique set of tax challenges. The state's tax laws are influenced by both federal guidelines and regional economic factors, creating a dynamic environment that demands attention. For individuals, this includes understanding income, sales, and property taxes. Businesses, on the other hand, must contend with corporate taxes, payroll deductions, and excise duties. This complexity often leads to confusion, making it essential to seek clarity through expert guidance or reliable resources.

This guide aims to simplify the process by breaking down key components of New York taxes into digestible sections. By exploring topics such as income brackets, deductions, credits, and compliance requirements, we provide a roadmap for achieving financial stability. Whether you're a newcomer to the state or a seasoned resident, this article will serve as your go-to resource for all things tax-related in New York.

Read also:Subhashree Sahu A Deeper Dive Into Her Life And The Controversy

What Are the Key Components of New York Taxes?

Before diving into specific details, it's important to understand the foundational elements of New York taxes. The state's tax system is multifaceted, encompassing various categories designed to generate revenue while ensuring equitable distribution. These include:

- State income tax: A progressive tax system based on income brackets.

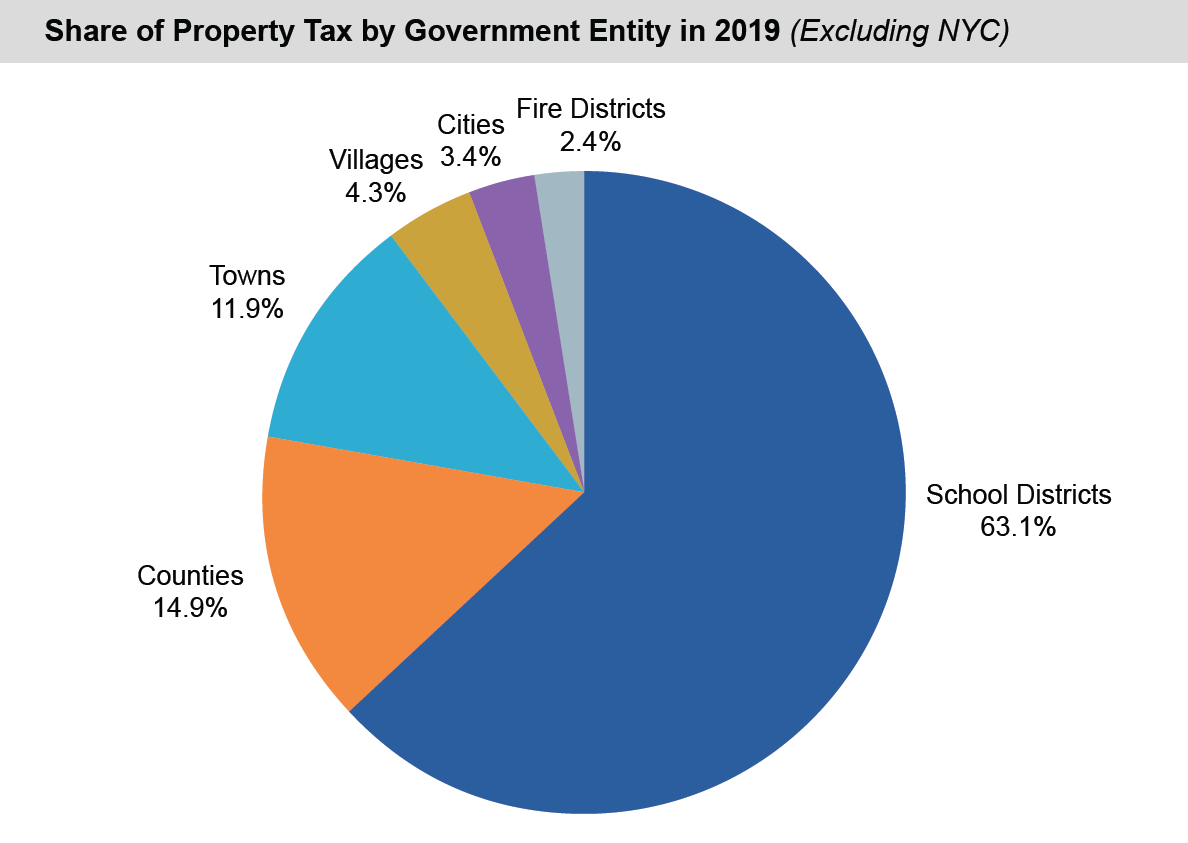

- Local property taxes: Varying rates depending on the municipality or county.

- Sales tax: A statewide rate supplemented by additional local surcharges.

- Excise taxes: Levied on specific goods and services, such as gasoline and cigarettes.

Each of these components plays a critical role in shaping the overall tax burden for individuals and businesses. Understanding how they interact is key to effective financial planning.

How Do Income Taxes Work in New York?

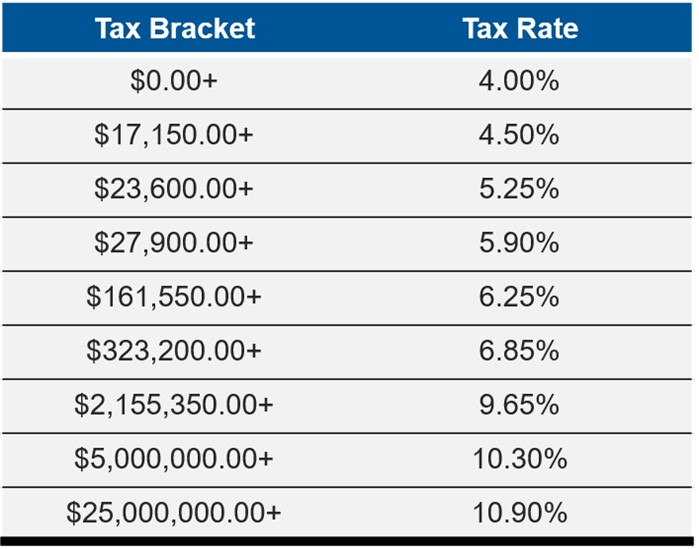

Income taxes in New York are structured on a progressive scale, meaning higher earners pay a larger percentage of their income. The state's tax brackets are updated annually to reflect inflation and economic changes. For instance, as of the latest updates, single filers earning up to $8,500 are taxed at 4%, while those earning over $1,077,550 face a top rate of 8.82%. These rates are subject to change, emphasizing the importance of staying informed.

Additionally, New York offers several deductions and credits to ease the burden. Examples include the Earned Income Tax Credit (EITC) for low-income workers and itemized deductions for mortgage interest and charitable contributions. Exploring these options can significantly reduce your taxable income and lower your overall liability.

What Are the Common Misconceptions About New York Taxes?

Many residents and businesses harbor misconceptions about New York taxes, leading to unnecessary complications or missed opportunities. One common myth is that all New Yorkers pay the same rate, ignoring the progressive nature of the system. Another misconception involves the belief that property taxes are uniform across the state, when in reality, rates vary widely based on location and property type.

Addressing these misunderstandings is vital for making informed decisions. By debunking myths and clarifying facts, individuals and businesses can better align their strategies with the realities of the tax landscape.

Read also:Joe Scarboroughs Resilient Journey A Comprehensive Update On His Health And Recovery

Why Are New York Taxes Higher Than Other States?

Compared to many other states, New York's tax rates are often perceived as higher. This perception is driven by several factors, including the state's large population, extensive public services, and high cost of living. Additionally, New York relies heavily on tax revenue to fund critical infrastructure projects, education, and healthcare initiatives. While this approach ensures robust public services, it also places a heavier financial burden on taxpayers.

What Are the Implications of New York Taxes for Businesses?

For businesses operating in New York, the tax environment presents both challenges and opportunities. Corporate taxes are assessed at a flat rate of 6.5%, but additional considerations such as payroll taxes and excise duties can increase the overall burden. To mitigate these costs, companies can leverage available credits and incentives, such as those for research and development or job creation.

Moreover, understanding the interplay between federal, state, and local taxes is essential for effective financial planning. Businesses that invest time in optimizing their tax strategies often find themselves in a stronger competitive position.

How Can Individuals Minimize Their New York Taxes?

Minimizing tax liabilities requires proactive planning and a thorough understanding of available deductions and credits. For individuals, this might involve maximizing contributions to retirement accounts, claiming education credits, or itemizing deductions. Consulting with a tax professional or leveraging tax preparation software can also streamline the process and ensure compliance.

Furthermore, staying informed about legislative changes is crucial. New York frequently updates its tax laws to address economic conditions or align with federal guidelines. Staying abreast of these changes allows individuals to adapt their strategies accordingly.

What Are the Deadlines for Filing New York Taxes?

Knowing the deadlines for filing New York taxes is essential for avoiding penalties and ensuring timely compliance. For individual income tax returns, the deadline typically aligns with the federal deadline, which is April 15th. Businesses, however, may have different deadlines depending on their structure and filing requirements. Extensions are available upon request, but it's important to note that these only extend the filing deadline, not the payment deadline.

How Do Local Taxes Impact New York Taxes?

Local taxes play a significant role in shaping the overall tax burden for New York residents. Property taxes, in particular, vary widely across municipalities, with some areas imposing significantly higher rates than others. Additionally, local sales taxes can add up to 4% or more to the statewide rate, depending on the location.

Understanding these variations is key to budgeting effectively and making informed decisions about where to live or operate a business. For instance, individuals considering a move within the state should research local tax rates as part of their decision-making process.

What Resources Are Available for Understanding New York Taxes?

Fortunately, numerous resources exist to help individuals and businesses navigate New York taxes. The New York State Department of Taxation and Finance website provides comprehensive guides, forms, and calculators. Additionally, consulting with a certified public accountant (CPA) or tax attorney can offer personalized advice tailored to your specific situation.

For those seeking self-guided learning, online courses and webinars are increasingly available. These resources cover everything from basic filing procedures to advanced strategies for reducing tax liabilities. Taking advantage of these opportunities can empower taxpayers to take control of their financial futures.

Conclusion: Mastering New York Taxes for Financial Success

Navigating the complexities of New York taxes requires knowledge, preparation, and adaptability. By understanding the key components, leveraging available resources, and staying informed about legislative changes, individuals and businesses can optimize their financial strategies. Whether you're filing your first tax return or restructuring your corporate finances, this guide serves as a valuable starting point for achieving success in the Empire State.

Table of Contents

- What Are the Key Components of New York Taxes?

- How Do Income Taxes Work in New York?

- What Are the Common Misconceptions About New York Taxes?

- Why Are New York Taxes Higher Than Other States?

- What Are the Implications of New York Taxes for Businesses?

- How Can Individuals Minimize Their New York Taxes?

- What Are the Deadlines for Filing New York Taxes?

- How Do Local Taxes Impact New York Taxes?

- What Resources Are Available for Understanding New York Taxes?

- Conclusion: Mastering New York Taxes for Financial Success